For the World Cup Final, will You replace Messi with a Local Club Player to lower wage costs?

Given the topical theme of the World Cup final, we’ll go with a soccer story today. For the World Cup final, do you think Argentina

“Many of you here are working on digitalisation projects but I would urge you to think bigger. You need to think about business model change – with existing customers or into whole new sectors. It isn’t just about product innovation. It’s about company innovation.”

Deborah Sherry at TM Forum Live!

I really like the way Deborah is thinking (she’s General Manager and Chief Commercial Officer of GE Digital Europe BTW).

On a different, but ultimately similar line of challenger-thinking, Eric Hoving also addressed TM Forum Live! with this statement, “We’ve spent zillions of dollars on BSS but who is in need of a bill? No over-the-top (OTT) company sends a bill and nobody ever uses the data of the billing system. Why do we have a billing system at all?”

So, I decided to follow those trains of thought by asking, “If telcos can’t issue bills, from where can they source new revenues? And in turn, will new revenue models drive entirely new telco business models?” Certainly BSS models would change because the revenue sources would change drastically.

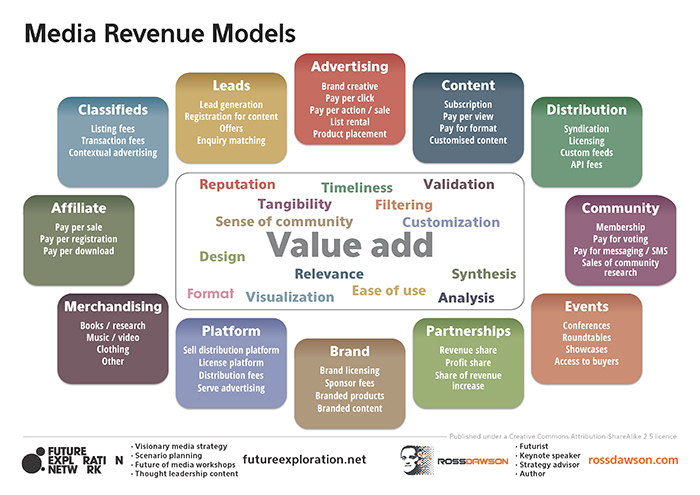

Whenever considering different revenue models, I refer back to this great image from Ross Dawson:

Now let’s break these down into ways OSS might contribute to alternative telco revenues:

Just one strong caveat on the thinking above and it was again brilliantly articulated by Eric Hoving at TM Forum Live!, “For 20 years we tried to make sense out of data and failed, but Google did it. Stuff is not an asset if you don’t get something out of it. If you aren’t going to do something with it then stop doing it.”

I’d love to hear your alternatives, your most innovative revenue / business model ideas!

PS. Check out this link from Sarah Wray that elaborates brilliantly on Deborah Sherry’s “Think Bigger” speech.

Given the topical theme of the World Cup final, we’ll go with a soccer story today. For the World Cup final, do you think Argentina

For decades, scale gave large telcos purchasing power, infrastructure reach, extensive capability and millions of customers. It became one of the world’s most powerful and

Success in business, distilled to its simplest form, is often about arbitrage. The gap between supply and demand. The gap between value delivered and value

When it comes to OSS, the term Out of the Box (or OOTB) can be correct, incorrect and highly confusing all at the same time.