What an OSS/BSS Procurement Really Costs: The Numbers Might Surprise You

An OSS/BSS transformation often begins with excitement and urgency due to a desperate need for change. It also creates trepidation because the wrong decision could

“The PayPal network, as it’s been called, is a set of friendships built over the course of a decade. It has become a sort of franchise. But this isn’t unique; that kind of dynamic arguably characterizes all great tech companies, i.e. last mover monopolies. Last movers build non-commoditized businesses. They are relationship-driven. They create value. They last. And they make money.”

Peter Thiel (actually a notes essay from Peter Thiel’s CS183: Startup – Class 3 lecture).

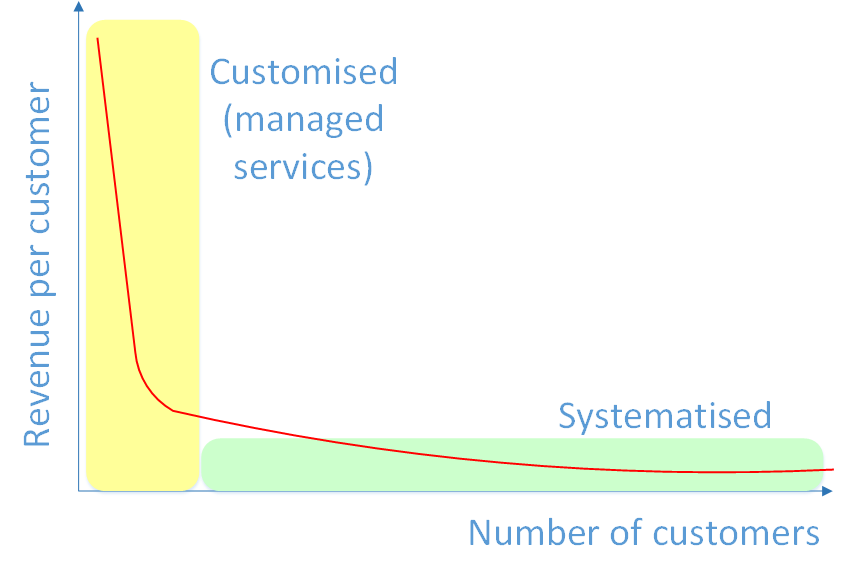

The OSS market is highly fragmented. The Leaders (the top right corner of the Gartner OSS Magic Quadrant) tend to service the Tier-1 CSPs exclusively and from my experience running vendor selections, of these vendors only one entertains bidding for customers from outside the top tier. To borrow from the long-tail diagram below, the Gartner Leaders primarily service only the yellow band.

The hundreds of other OSS vendors supply to a combination of yellow and green bands, either servicing functional niches (eg root cause analytics) or perhaps customer-type niches (eg power companies).

Given this fragmentation, OSS has yet to be dominated by an organisation that fits Peter Thiel’s last mover monopoly classification. In OSS we don’t have what Google is to search, Amazon is to online retail, etc.

Can you think of an organisation that fits all of the following criteria based on their OSS solutions alone?

“They are relationship-driven. They create value. They last. And they make money.”

Tomorrow we look at some further insights of Peter Thiel and see what factors might allow a last mover monopoly to emerge in the OSS industry.