For the World Cup Final, will You replace Messi with a Local Club Player to lower wage costs?

Given the topical theme of the World Cup final, we’ll go with a soccer story today. For the World Cup final, do you think Argentina

When it comes to driving efficiency and profitability in a service provider’s business, I feel there are three key pillars to consider (aside from strategic factors of course), as follows:

The networks are vital. They are effectively each organisation’s product because connectivity across the network is what customers are paying for. They must be operating effectively to attract and retain paying customers.

The field services are vital. They build and maintain the networks, ensuring there is a product to sell to customers.

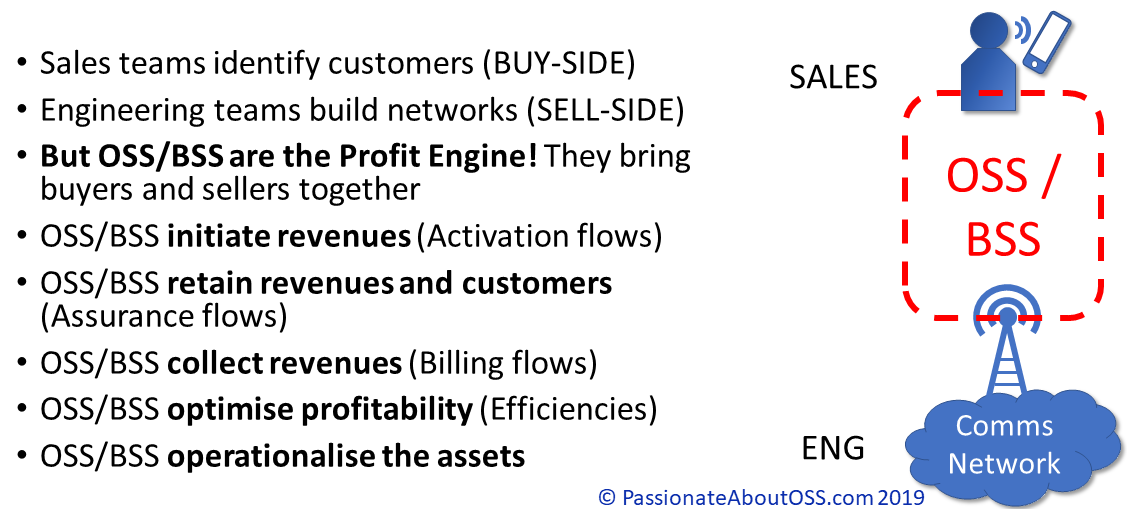

The OSS/BSS are arguably even more vital. Some may argue that they only provide a support role (the middle S in OSS and in BSS would even suggest so!). They’re more than that. OSS/BSS are the Profit Engine of a service provider.

But let’s take a closer look at the implications of effectiveness and profitability in the overlapping sectors in the Venn diagram above and why OSS/BSS are so important.

Sector 1. OSS / BSS <-> Networks

The OSS/BSS connects customers with the product (buyers with sellers). Even if we remove this powerful factor, OSS and BSS have other key roles to perform. They connect and coordinate. They hold the key to efficiency and utilisation and, in turn, profitability.

Sectors 2&3. OSS / BSS <-> Field Workforce and Network

The OSS/BSS manages the field workforce, assigning what to do and when. But before that, our OSS/BSS provide the tools to decide why the work needs doing. They identify:

That covers sector 2. But sector 3 appears to be separated from the OSS/BSS. It is, the field workers work directly on the network. However, they generally only do so after direction from the OSS/BSS (eg via work orders, trouble tickets, etc). Hence, they’re merged here.

Summary – Efficiency and The Profit Engine

You might be wondering why I missed sector 4. You might also be wondering whether the last sentence above, with the OSS/BSS pulling the strings of field work on networks, represents sector 4. Well, yes, but be patient and we’ll come back to sector 4, but with a slightly different (and potentially more powerful) perspective than that.

From the two previous sections, you would have noticed just how important OSS and BSS are to a network service provider. They directly influence:

When you consider the daily volumes of each of those factors at large telcos, you’ll understand how a 5% improvement or deterioration in any will have a significant implication on profitability. The profitability of an organisation is massively helped, or hindered, by OSS/BSS, though few people seem to realise it.

The Elusive Sector 4. Combining OSS/BSS, Network and Field Services.

I promised to come back to sector number 4 in the Venn diagram above and give a different perspective. There’s an opportunity that exists here that few are capitalising on yet.

But first a recap. Sector 1 is best characterised by the tools used by a NOC (Network Operations Centre) and SOC (Service Operations Centre), as well as their various metrics like time to repair, up-time / availability, etc.

Sectors 2 and 3 are best characterised by the tools used by a WOC (Workforce Operations Centre) and metrics like number of truck rolls, jobs completed, etc.

The analytics that are available at sector 4 are profound, but rarely used. Let me describe via a scenario:

The OSS/BSS has the ability to provide the role as an overseer, observing not just the transaction metrics, but also considering effectiveness and profitability. It is able to consider:

With all of this knowledge at the fingertips of the OSS/BSS, it could decide to inject a new work order into the work queue, starting with a network design (possibly automated), acquisition of assets / materials (possibly automated), notification to customers of network uplift (resulting in outage notifications, but also better performance and higher-speed offerings – possibly automated), creation / scheduling / dispatch of jobs to deconstruct / construct / commission infrastructure in region A, then notify customers of availability of service.

The metrics that matter at sector 4 are less about transactions and more about higher-order objectives like effectiveness and profitability. It also has the potential to take a longer-term view to align short-term decisions with long-term objectives (eg technology objectives such as “fibre deeper” [ie fibre being extended closer to end-users to facilitate higher bandwidth services], CAPEX/OPEX optimisation for ROI, network footprint changes, etc).

In many cases, network operators don’t have these near-real-time decision support tools at hand. If network uplift is to be performed, it’s decided across an entire service area by capacity planning teams rather than in more granular regions.

This is only one scenario for what could be achieved at sector 4. I’m sure we can imagine more if we start building the tools here.

Also consider the different speeds that the OSS/BSS need to cater for and optimally allocate as part of end-to-end workflows:

Given the topical theme of the World Cup final, we’ll go with a soccer story today. For the World Cup final, do you think Argentina

For decades, scale gave large telcos purchasing power, infrastructure reach, extensive capability and millions of customers. It became one of the world’s most powerful and

Success in business, distilled to its simplest form, is often about arbitrage. The gap between supply and demand. The gap between value delivered and value

When it comes to OSS, the term Out of the Box (or OOTB) can be correct, incorrect and highly confusing all at the same time.