The Age-Old IT vs OT Debate: Who gets the Keys to Your OSS?

For decades, organisations have argued over whether IT or operations (OT) teams should control the OSS environment, as though it’s a binary decision. Giving one

Since widespread deregulation of telecommunications globally, the passing of data has become a commodity. Perhaps it always was, but increased competition has steadily driven down dollar per bit. It’s likely to continue on that path too. Meanwhile the expected throughputs and consumption of data services is ramping ever-upwards, which requires investment in networks by their operators.

By definition, a commodity is a product/service that is indistinguishable between providers. The primary differentiator is price because there are no other features that make a buyer choose one provider over another.

At face value, that’s true of commodities such as oil or iron ore, just as it is for data. What could be less differentiated than ones and zeroes?

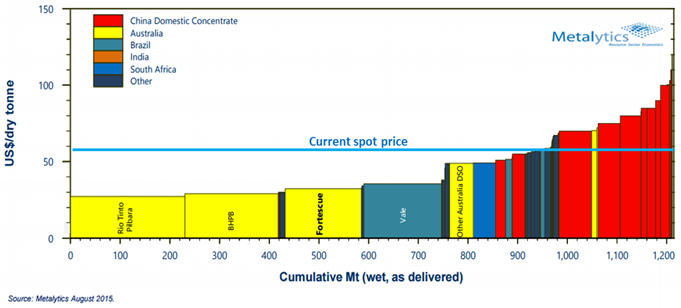

However, as the charts below show for oil and iron ore, commodities aren’t always a level playing field. Some suppliers have significant differentiation – via cost of production advantages over their competitors.

What if we created a $/bit graph of telcos similar to the oil graph above showing opex and capex splits? Which countries / operators would have significant advantage? Which telcos are like Rio Tinto, comfortable in the knowledge that no matter how low the spot price goes, their competitors will be deeply unprofitable (and possibly out of business) long before they will be.

Virtualisation of network infrastructure (SDN, NFV, cloud) has been the much-hyped saviour of telco business models. However, like me, you’ve probably started hearing news that savings from these architectures just aren’t eventuating. Cost-bases are possibly even going up because of their increased complexity. Either way, incremental cost reduction tends to have diminishing returns anyway.

It would seem that telcos are left with two / three choices:

OSS/BSS has a part to play with both of these options.

Structurally lower cost comes not from cost reduction but from having far simpler variant trees (ie smaller numbers of product offerings, network types, system integrations, service configuration styles, support models, obsolescence of legacy / grandfathered products, minimal process options, etc, etc). Some of this happens within the OSS/BSS, but a lot more of it stems from upstream decisions.

Differentiation / innovation means being able to innovate through experiences / insights / content / trust / partnerships / ecosystems / local-presence in ways that other organisations can’t. It’s unlikely to be in software alone or in cloud infrastructure because others have proven to do that far more effectively than telcos. As much as they wish otherwise, it’s just not in the DNA of many. Yet that’s where most attention seems to be. Meanwhile OSS/BSS are waiting to be the glue that can leverage the competitive advantages that telcos do still hold.

For decades, organisations have argued over whether IT or operations (OT) teams should control the OSS environment, as though it’s a binary decision. Giving one

Given the topical theme of the World Cup final, we’ll go with a soccer story today. For the World Cup final, do you think Argentina

For decades, scale gave large telcos purchasing power, infrastructure reach, extensive capability and millions of customers. It became one of the world’s most powerful and

Success in business, distilled to its simplest form, is often about arbitrage. The gap between supply and demand. The gap between value delivered and value